Finance and fintech organizations face a threat landscape shaped by the value of what they protect: sensitive financial data, account credentials, payment infrastructure, and the trust of customers whose financial well-being depends on platform integrity. That combination of high-value assets and complex regulatory obligations makes this one of the most consistently and thoroughly tested sectors in our portfolio.

In our 2025 Annual Penetration Testing Review, we analyzed 3,294 confirmed vulnerabilities across 660 penetration tests covering 145 organizations from 11 industries.

Finance and Fintech was the second largest sector by testing volume: 34 financial firms commissioned 187 separate penetration testing engagements, generating 841 confirmed security findings.

This article draws on that data to examine the common vulnerabilities in finance and fintech environments, the types of assessments driving those findings, and what the patterns tell us about where this sector’s risk is actually concentrated.

Why Finance & Fintech Tests So Often

At 187 projects and 841 findings, Finance & Fintech is the second most tested sector in our dataset, behind only e-commerce and retail. The 4.50 average vulnerabilities per project sits slightly below the cross-sector mean of 4.99 — a figure consistent with a sector that tests frequently and at depth.

The high project volume reflects the regulatory environment as much as technical complexity. Finance and fintech organizations typically operate under compliance frameworks — PCI DSS, DORA, SOC 2, ISO 27001 — that mandate regular security testing as part of audit programs. This creates a testing cadence that is partly driven by compliance obligations rather than purely by perceived risk.

Financial technology organizations in particular combine the sensitive data handling with the rapid development cycles of technology companies — a combination that generates both a broad attack surface and frequent code changes that require recurring security validation.

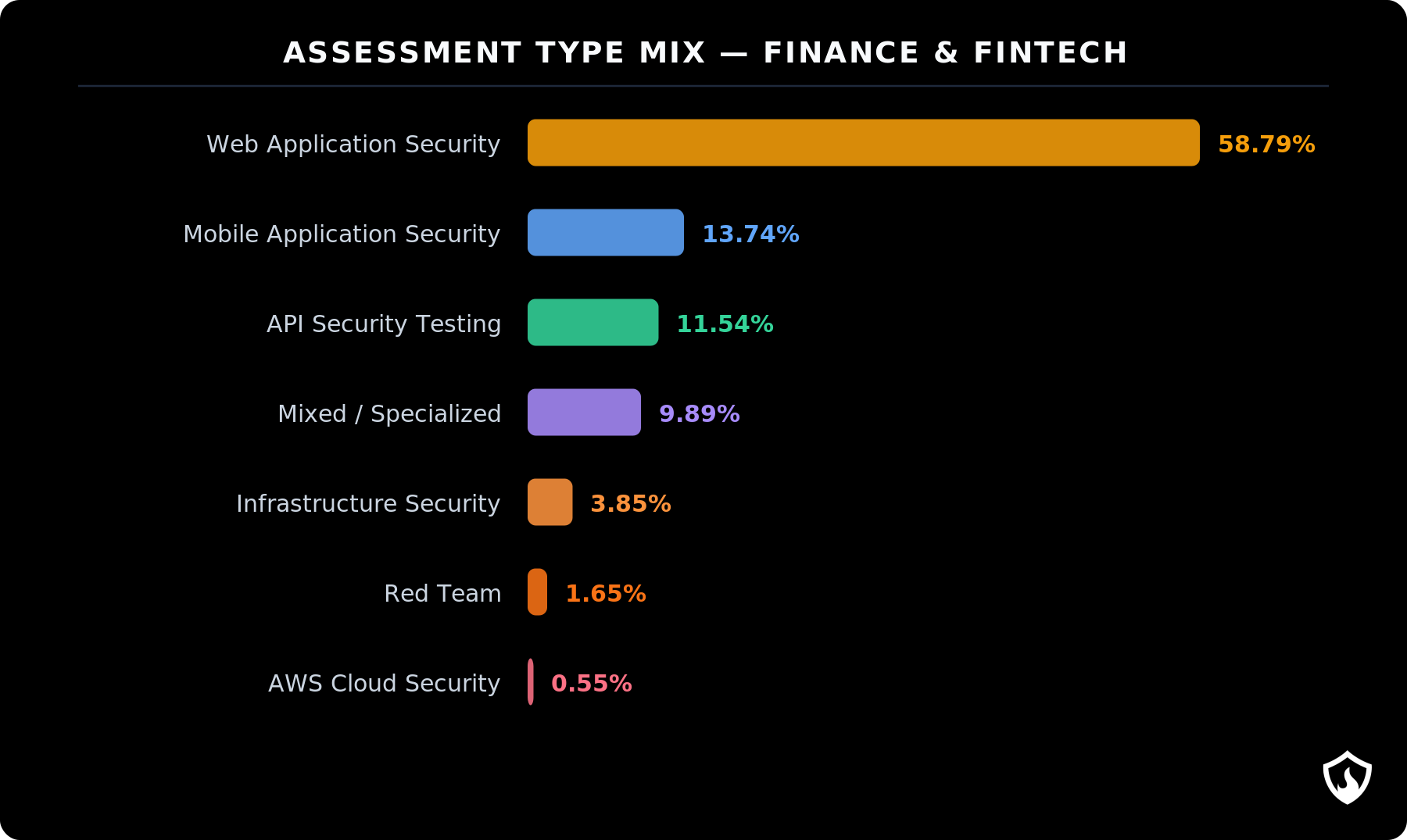

The Assessment Mix: Mobile Testing Stands Out

Finance & Fintech has the highest mobile application testing share of any sector in our dataset at 13.74%. Web application testing leads at 58.79%, and API security testing accounts for 11.54%.

The mobile prominence reflects the sector’s product reality. Mobile banking apps, payment wallets, trading platforms, and authentication flows are central to fintech user journeys. Unlike e-commerce, where APIs handle back-end commerce logic across third-party integrations, fintech mobile apps often contain the entire customer experience — account management, transfers, authentication, and compliance flows — making mobile security a front-line concern rather than a secondary surface.

API testing at 11.54% is meaningful but significantly lower than e-commerce’s 31.4%. Finance platforms tend to use APIs for internal service-to-service communication more than for broad third-party integration, which changes both the API attack surface and the appropriate testing methodology.

The remaining share covers mixed or specialized assessments (9.89%), infrastructure security (3.85%), red team engagements (1.65%), and cloud assessments (0.55%). The red team share indicates that some finance organizations are testing cyber resilience beyond individual application layers — a maturity signal consistent with the sector’s regulatory pressure.

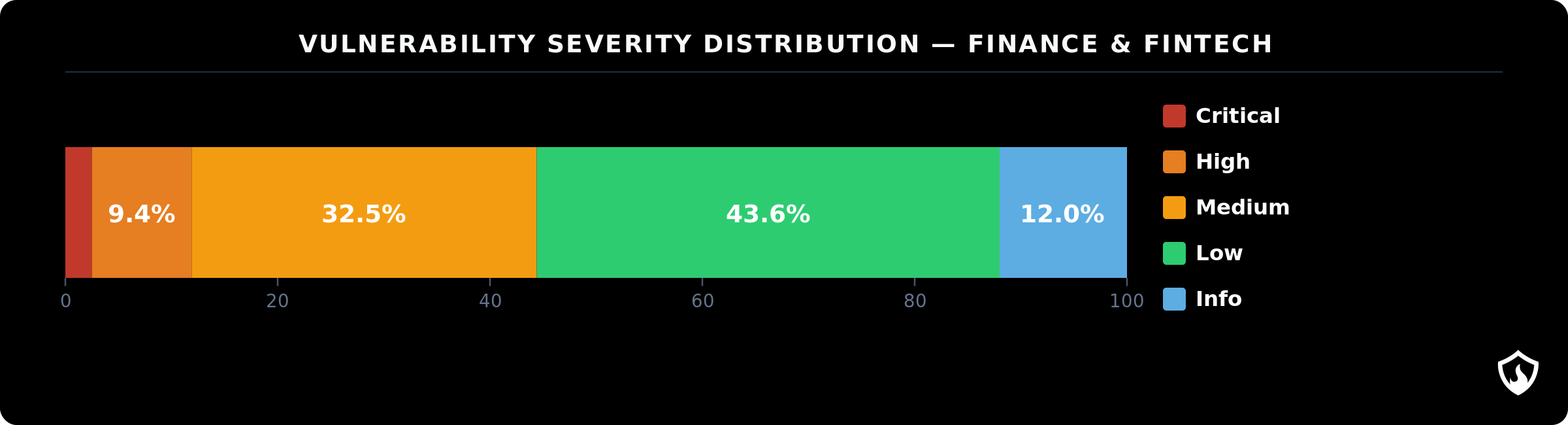

Severity Profile of Finance Pentest Findings

Across 187 projects and 841 findings, the average number of vulnerabilities per project was 4.50. The severity distribution shows: 43.6% Low, 32.5% Medium, 12.0% Informational, 9.4% High, and 2.5% Critical.

The combined High and Critical rate of 11.9% is low relative to sectors like Education (32.0%), Public Services (29.2%), and Insurance (27.6%), but slightly higher than e-commerce (9.1%). This is consistent with a sector that tests frequently and at depth, catching issues before they accumulate into critical debt.

What stands out in comparison to peer sectors is that Finance & Fintech shows a higher severe finding rate than e-commerce (11.9% vs 9.1%) despite similar testing frequency and volume. Both sectors test at scale and at depth. The gap suggests that financial system complexity — legacy components, internal service meshes, and privileged infrastructure — generates architectural risks that persist even in mature security testing programs.

The 2.5% Critical rate merits attention in absolute terms: across 841 findings, approximately 21 were Critical severity — each representing a confirmed, exploitable weakness in an environment where consequences may include financial loss, regulatory breach, or compromise of payment processing capabilities.

The dominance of Medium findings at 32.5% reflects a sector where security controls are broadly in place but inconsistently applied across workflows — a pattern that runs throughout the top vulnerability findings.

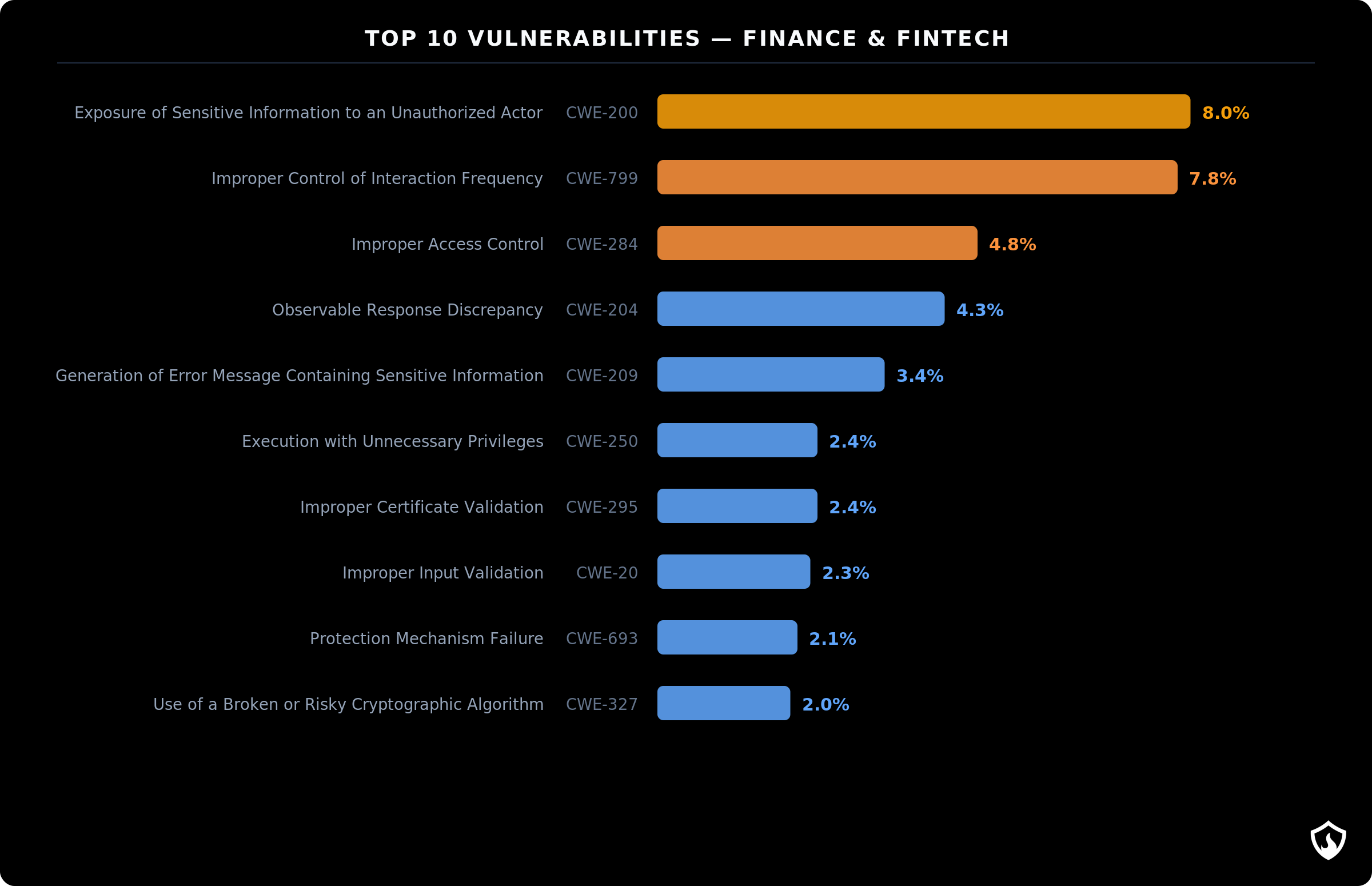

The Top 10 Vulnerabilities: Patterns Worth Understanding

Two things stand out before examining the clusters. First, the #1 and #2 findings are virtually tied — CWE-200 at 8.0% and CWE-799 at 7.8%, separated by just 0.2 percentage points. In every other sector in our dataset, CWE-200 leads by a clear margin. The near-tie reflects something specific about fintech’s fraud exposure profile. Second, the bottom five findings (positions 6–10) all land between 2.0% and 2.4% — an unusually compressed range suggesting broad, distributed exposure across control categories rather than a few dominant secondary issues.

Information disclosure

CWE-200 (8.0%), CWE-204 (4.3%), and CWE-209 (3.4%) together account for approximately 15.7% of sector findings. In financial environments, these weaknesses carry disproportionate weight: account numbers, transaction histories and identity verification details are immediately monetizable, and data leaks in this sector tend to have direct fraud consequences rather than disclosure-only impact. CWE-204’s response discrepancy pattern is particularly relevant in fintech — it creates a reliable channel for account enumeration at scale across login flows and password reset mechanisms processing high volumes of authentication events.

Access control and interaction limits

At 7.8%, CWE-799 is not a hygiene item in this sector — it is the technical precondition for the credential stuffing, transaction flooding, account enumeration and social engineering attacks that drive financial fraud. CWE-284 (4.8%) remains the most consistently severe vulnerability class across all industries we assessed, manifesting in fintech at the account, administrative, and service-permission levels. CWE-250 (2.4%) — processes running with unnecessary privileges — rounds out a cluster that accounts for approximately 15.0% of findings and is largely invisible to perimeter-focused testing.

Cryptographic, validation, and protection failures

CWE-295 (Improper Certificate Validation, 2.4%) appears in the Finance & Fintech top ten but not in most other sector top tens — pointing to failures in internal service-to-service certificate verification where mTLS should be standard. CWE-20 (2.3%), CWE-693 (2.1%), and CWE-327 (2.0%) complete a cluster where controls exist but are implemented inconsistently. In environments where cryptographic integrity protects transaction records and audit trails, the 2.0% floor on these findings carries risk disproportionate to its percentage. Together, this cluster accounts for approximately 8.8% of findings.

How These Vulnerabilities Are Reached

Pentest findings in the financial sector are overwhelmingly network-based, but this sector shows a higher proportion of local attack vectors than most others — reflecting the presence of internal systems, privileged administrative interfaces, and operational tooling specific to financial infrastructure. Vulnerabilities frequently require no user interaction, lowering the bar for threat actors considerably, but a meaningful subset assumes some level of authentication, pointing to flaws discovered post-login rather than purely at the perimeter.

Compared to other industries, Finance & Fintech shows an elevated impact across both confidentiality and integrity. Most sectors skew heavily toward confidentiality loss; findings primarily expose data. In financial environments, the elevated integrity impact signals vulnerabilities that could allow transaction manipulation or record modification, not just data theft. That is a materially different consequence class — one that carries direct financial loss exposure rather than disclosure risk alone. Scope change remains rare, indicating that most findings affect individual components rather than cascading across trust boundaries, but the integrity dimension means the blast radius of individual findings may be larger than their severity rating suggests.

What This Means for Security and Engineering Teams

Mobile security deserves the same rigor as web security

At 13.74% of testing volume, mobile applications represent the highest mobile share of any sector we assessed. Mobile apps in fintech often contain the full customer experience — authentication, transfers, account management, and compliance flows. Mobile-specific vulnerabilities around certificate validation, credential handling, and session management require a dedicated testing methodology, not inclusion as an afterthought in web assessment programs.

Rate limiting is a financial fraud control, not just a security hygiene item

CWE-799 at 7.8% — virtually the top finding — reflects a sector where abusive traffic directly enables fraud: credential stuffing, account takeover, transaction flooding, and enumeration of customer accounts. Rate-limiting gaps in fintech are not theoretical; they are the technical preconditions for fraud patterns that carry direct financial and regulatory consequences.

The 2.5% Critical rate understates the risk concentration

While the overall severity distribution looks controlled, roughly 21 Critical findings across 841 represent confirmed, exploitable weaknesses in environments where consequences include financial loss, regulatory penalty, and loss of payment processing capabilities. Individual critical findings in this sector warrant faster remediation timelines than portfolio averages might suggest.

Testing must follow the product, not just the perimeter

The range of assessment types — from web and mobile to red team and cloud — reflects a sector where cyber risk lives across the entire product surface. Perimeter-focused testing misses post-authentication access control failures, mobile session handling weaknesses, internal privileged access patterns, and the certificate validation issues in service-to-service communication that appear most frequently in our data.

About This Data

All penetration testing findings were collected through VulnKeep, Blaze’s penetration testing-as-a-service (PTaaS) platform, and represent confirmed, validated vulnerabilities identified during live security assessments — not theoretical risks or automated scan results.

Want to benchmark your finance or fintech platform against these findings? Our team runs web applications and API, mobile, and infrastructure security assessments tailored to financial environments, with findings delivered in real time through our pentest-as-a-service platform. Get in touch to discuss a testing program that fits your compliance calendar and release cadence.

FAQ

What are the most common security vulnerabilities found in fintech applications?

Based on Blaze’s 2025 data, the most frequent findings in fintech environments are information exposure (CWE-200), rate limiting failures (CWE-799), and improper access control (CWE-284). These three clusters account for over 30% of all findings in the sector. What distinguishes fintech from other industries is the near-equal prominence of rate limiting and information disclosure at the top — a pattern that directly maps to the credential stuffing and account enumeration techniques used in financial fraud.

How does fintech penetration testing differ from other industries?

Finance and fintech engagements tend to include a higher proportion of mobile application testing than any other sector, reflecting the central role of mobile apps in banking and payment products. Testing also more frequently involves post-authentication scenarios, internal service communication, and privileged infrastructure components that don’t appear in standard web perimeter assessments. Red team engagements, absent from most other sectors, appear in the fintech mix as organizations test organizational resilience alongside application security.

How often should fintech companies perform penetration testing?

The answer depends partly on compliance obligations — PCI DSS, DORA, SOC 2, and ISO 27001 each carry different testing frequency requirements. Beyond compliance, our data suggests that sectors with higher testing cadence consistently show lower rates of critical and high-severity findings. For fintech organizations running frequent deployments or managing multiple products, a continuous or quarterly testing program tied to release cycles is more effective than an annual point-in-time assessment.