Financial institutions in 2026 are being attacked through the systems and relationships that make modern finance work: digital identity, remote access, SaaS platforms, payment workflows, cloud infrastructure, customer devices and third-party providers.

That makes the threat picture harder to reduce to a single malware family or actor group. The more useful question is where attackers can create leverage: by stealing data, disrupting availability, abusing trusted access, compromising suppliers, impersonating executives or taking over customer accounts.

ENISA’s 2025 Threat Landscape report reflects this shift. Finance represented a relatively small share of collected EU cyber incidents, but a much larger share of incidents with significant impact. The financial sector also saw a mix of hacktivist disruption, cybercrime and state-aligned activity, with banks remaining the most exposed subsector.

This article breaks down the biggest cyber threats in finance in 2026, how they are changing, who is driving them, and what cybersecurity, risk and resilience teams should prioritize.

Four shifts shaping financial cyber threats in 2026

Modern finance is being attacked through trust relationships: identities, suppliers, customer channels, SaaS platforms and shared infrastructure. Four shifts explain why the threat landscape is becoming harder to contain:

- Identity and edge systems are the new front door. Attackers are targeting VPNs, remote-access tools, SaaS logins, identity providers, cloud consoles and internet-facing applications.

- Ransomware is becoming data extortion. Encryption still matters, but stolen data, disclosure pressure and regulatory exposure increasingly create the leverage.

- Shared technology providers are creating concentration risk. Shared cloud, SaaS, identity, file-transfer and financial technology providers can turn one supplier issue into exposure across multiple institutions.

- Cybercrime, fraud and state activity are converging. Infostealers, fake workers, SaaS abuse, extortion and identity theft now appear across both criminal and state-aligned operations.

What are the biggest cyber threats to financial institutions in 2026?

The sections below translate those shifts into practical threat categories, focusing on how each one creates operational, financial or trust impact for financial institutions.

1. Data extortion and ransomware attacks

Data extortion remains one of the most damaging cyber threats in finance. Ransomware operators increasingly rely on stolen data, regulatory pressure and reputational impact rather than encryption alone.

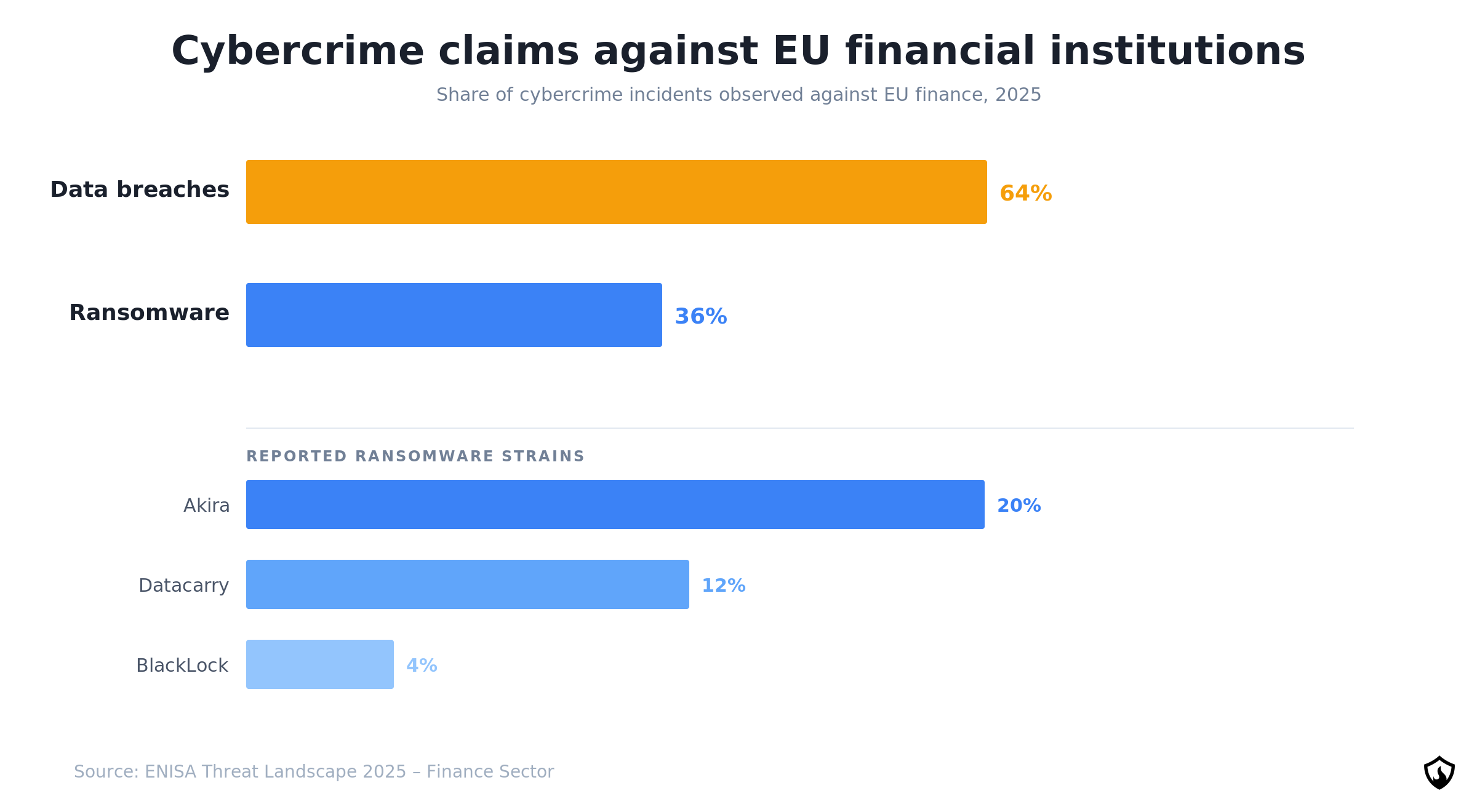

According to ENISA, cybercrime claims against EU financial institutions were more often linked to data breaches than ransomware: data breaches accounted for 64%, while ransomware accounted for 36%. The named ransomware strains reported against EU financial institutions were Akira, Datacarry and BlackLock.

Akira is the clearest public case study because its access patterns map closely to finance-sector controls: VPN exposure, MFA gaps, known vulnerabilities, valid credentials, external-facing services and data exfiltration. A joint FBI/CISA advisory reported that Akira had claimed approximately $244.17 million in ransomware proceeds by late September 2025 and described incidents where data was exfiltrated in just over two hours from initial access.

2. Third-party and concentration risk

Third-party risk has become concentration risk in financial services. Banks, insurers and payment firms increasingly depend on a relatively small set of cloud providers, SaaS platforms, identity systems, file-transfer products and specialist financial-technology vendors for critical operations.

The pattern is not new. Cl0p/MOVEit showed how exploitation of a widely used file-transfer product can turn into bulk data theft across many organizations. Snowflake showed a different version of the same risk: the provider’s core environment was not found to be breached, but compromised customer credentials, weak MFA coverage and SaaS configuration gaps still created large-scale exposure.

More recent finance-sector cases, including SitusAMC and Chain IQ, show why the issue remains current. The risk is no longer only whether a supplier can be breached, but how much operational exposure, data access and dependency can accumulate around shared technology providers.

3. Identity compromise and access abuse

Identity compromise remains one of the most reliable intrusion paths into financial institutions. Attackers can gain access by abusing trusted identities through phishing, stolen credentials, session hijacking, MFA interception, help desk manipulation and compromised remote access workflows.

Adversary-in-the-middle phishing is especially important because it weakens the assumption behind traditional MFA. The attacker is not only collecting a password; they are relaying the login in real time, capturing the authenticated session and using that access before activity appears suspicious.

The Federal Reserve’s 2025 Cybersecurity and Financial System Resilience Report highlights the evolution of phishing attacks in financial services, including QR code phishing that directs users into less-monitored mobile contexts and real-time one-time password interception via adversary-in-the-middle infrastructure. Scattered Spider remains the clearest actor example: its tradecraft targets help desk workflows, MFA reset procedures, contractor onboarding, device registration and privileged-access escalation.

Blaze’s penetration testing of finance and fintech environments shows the same pattern in practice: exposed services, authentication weaknesses and access-control gaps remain common paths from initial access to wider compromise. See our analysis of common penetration testing findings in finance and fintech.

4. AI-enabled impersonation and fraud

Generative AI is accelerating impersonation-driven fraud across the financial sector. The most immediate impact is not autonomous cyberattacks, but the ability to generate convincing phishing messages, cloned voices, fake video interactions and localized payment or support scams at scale.

The Federal Reserve’s report highlights three developments especially relevant to finance: AI-generated phishing content that is more believable and multilingual; voice cloning capable of defeating weak verification controls; and the use of jailbroken or criminally tailored AI models to support fraud and social engineering.

North Korean remote IT worker schemes show how these techniques are already being operationalized. In 2025, the FBI warned that DPRK-linked workers used AI-enhanced identity manipulation and face-swapping technology during remote hiring processes. For financial organizations, the control issue is clear: voice, video and written communication can no longer be treated as reliable proof of identity.

5. Distributed Denial of Service and availability disruption

DDoS attacks remain operationally significant in finance because service availability is part of customer trust and market confidence. If customers cannot access online banking, payment portals, insurance platforms or trading services, the impact is immediate, even when no data is stolen.

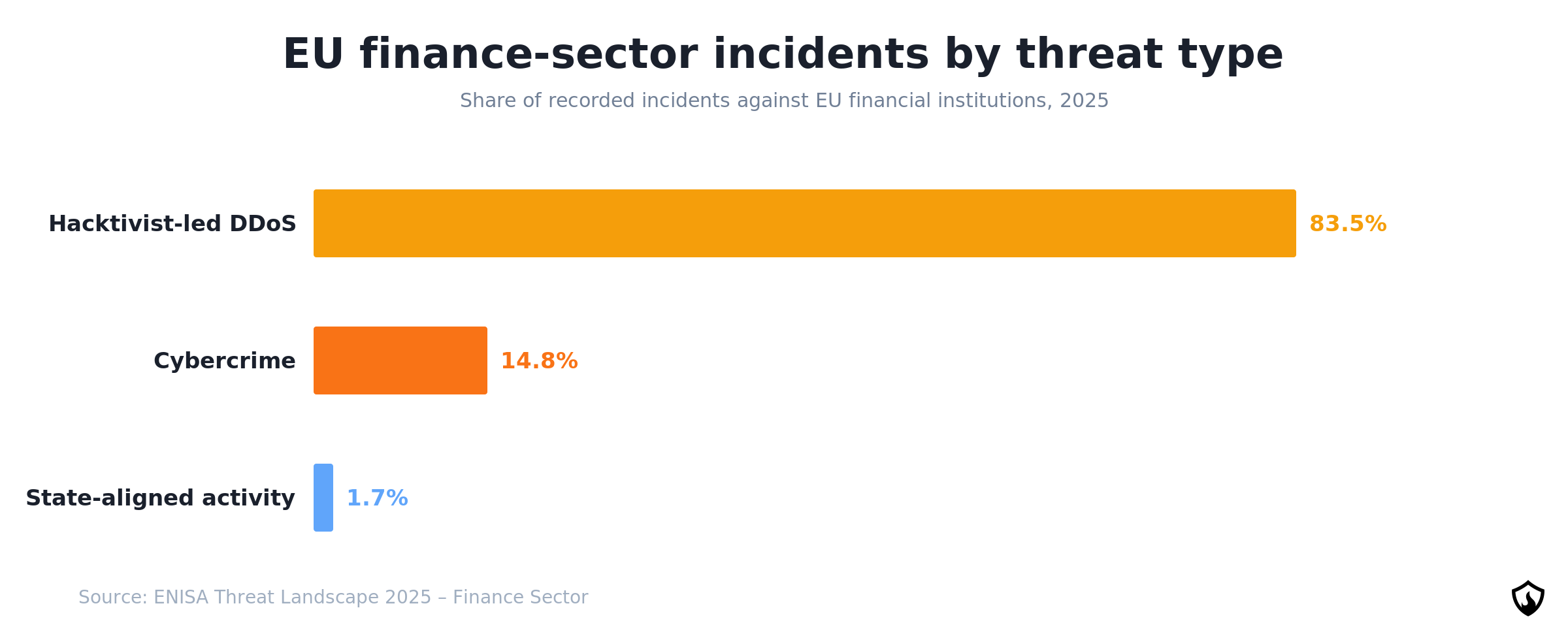

ENISA found that hacktivist-led DDoS made up 83.5% of recorded EU finance-sector incidents in its dataset. Banks were the most targeted finance subsector by hacktivist groups, accounting for 69% of hacktivist targeting in the sector.

The most active groups recorded against the financial industry were NoName057(16), DarkStorm Team and Keymous+. The Federal Reserve adds that major anti-DDoS providers remain reasonably well-positioned against high-volume attacks, but the dark-web market for DDoS services has expanded, lowering the barrier for less capable cyber criminals.

6. Customer-channel compromise and account takeover

Some of the most persistent cybersecurity threats in finance originate through customer channels rather than direct compromise of the institution itself. Attackers use phishing, smishing, malicious mobile applications, abused remote-access tools and banking trojans to hijack trusted customer sessions and perform fraudulent transactions.

ENISA’s 2025 Threat Landscape documents a resurgence of Android banking trojans across European member states, including Octo/Octo2, Medusa and BingoMod. These families are relevant because they support on-device fraud, where malicious activity may appear to originate from the legitimate user’s own device, session and behavioral profile.

For banks and payment providers, the challenge is that one attack chain may involve smishing, theft of credentials, device compromise, abuse of remote-access tools, mule-account activity and customer service contact. Treating these as separate events slows detection and response.

7. State-aligned and hybrid threat activity

Financial institutions remain strategic targets for state-aligned actors because they sit close to sanctions enforcement, payment infrastructure, financial intelligence, cryptocurrency flows and critical economic systems.

The distinction between nation-state operations and financially motivated cybercrime is becoming less clear. State-linked groups increasingly adopt cybercriminal techniques such as theft of credentials, contractor impersonation, SaaS abuse, extortion and infostealer operations.

In 2025, the dominant state threat to financial organizations continued to be North Korea, especially Lazarus, linked publicly to cryptocurrency theft, fraudulent remote IT-worker schemes, data extortion and revenue generation. Relevant financial sector threat models should also include China, Russia and Iran-linked groups whose activity intersects with payment infrastructure, cloud and identity systems, critical infrastructure, executive targeting, sanctions-linked operations and politically timed disruption.

Threat actors targeting financial institutions

Advanced persistent threats and state-aligned actors are not the only threats to the financial sector. The table below features threat actors and categories of threats that are relevant to the financial services sector:

| Actor or category | Type | Why it matters to finance |

|---|---|---|

| Akira | Ransomware and data extortion | Named by ENISA as the largest reported ransomware strain against EU financial sector; associated with VPN abuse, valid credentials, exposed services and data exfiltration |

| Datacarry | Ransomware strain | Reported by ENISA among ransomware strains affecting EU financial institutions |

| BlackLock | Ransomware strain | Reported by ENISA among ransomware strains affecting EU financial institutions |

| Cl0p / TA505 | Mass exploitation and data extortion | Relevant because of repeated exploitation of widely used enterprise platforms, including file-transfer products |

| Scattered Spider | Identity-led cybercrime and social engineering | Targets help desks, MFA reset processes, credential theft, contractor workflows and privileged access |

| NoName057(16) | Hacktivist DDoS group | Dominant hacktivist group in ENISA’s EU finance-sector DDoS data |

| DarkStorm Team | Hacktivist DDoS group | Associated with politically timed availability disruption |

| Keymous+ | Hacktivist DDoS group | Reported by ENISA among the most active hacktivist groups targeting EU finance |

| Lazarus / DPRK nexus | State-aligned, financially motivated | Relevant because of cryptocurrency theft, financial targeting, sanctions evasion and revenue-generation operations |

| DPRK IT-worker schemes | Fraudulent workforce and insider-access threat | Fraudulent workers can gain legitimate access to code, cloud systems, internal tools and sensitive data |

| Silver Fox / Void Arachne | China-aligned, dual-purpose activity | Named by IBM as conducting both intelligence-driven and financially motivated operations |

| Initial-access brokers / infostealers | Cybercrime enablers | Convert stolen credentials, session tokens and compromised endpoints into sellable access |

What about quantum cryptography?

Post-quantum cryptography is not an immediate operational threat in the same way as ransomware or DDoS, but it is already a planning issue for financial institutions.

The Federal Reserve flags this directly in its 2025 report: future quantum capabilities could render the asymmetric encryption standards used pervasively across financial services obsolete, and finance-sector data tends to have a long-lived value horizon — meaning encrypted data captured today can be decrypted in the future once a relevant quantum capability exists.

NIST finalized its first three post-quantum encryption standards in August 2024 and encouraged system administrators to begin transitioning.

Cyber resilience priorities for financial organizations in 2026

Financial institutions cannot prevent every attack, but they can reduce the paths most likely to lead to material impact. The highest-value priorities are:

- Reduce exposure at the edge: continuously inventory and patch internet-facing applications, VPNs, remote-access appliances, file-transfer tools, cloud management interfaces and APIs — addressing the 36% of finance-sector intrusions that begin with public-facing-application exploitation according to IBM X-Force Threat Intelligence Index 2026.

- Treat identity as critical infrastructure: prioritize phishing-resistant MFA, hardware-bound credentials, conditional access, device trust, privileged access management and help-desk verification.

- Design ransomware response around data extortion: test exfiltration assessment, leak-site pressure, regulator engagement, customer notification, communications and payment decision governance.

- Test supplier compromise and failure: exercise scenarios involving SaaS platforms, identity providers, managed service providers, file-transfer products, endpoint tools and cloud dependencies.

- Make payment and access workflows deepfake-resistant: require out-of-band verification, dual approval and hard procedural limits for sensitive payment, beneficiary and access changes.

- Build cyber-fraud fusion: connect cyber, fraud, digital banking and customer-support telemetry around account takeover, smishing, mule activity and payment manipulation.

- Improve triage of commodity-looking alerts: do not automatically deprioritize alerts involving privileged accounts, unusual remote access, SaaS exports, data staging or contractor behavior.

- Secure contractor and remote-worker access: strengthen identity verification, device control, least privilege, code repository monitoring and staffing-firm assurance.

- Use threat-led testing: test realistic scenarios involving edge exploitation, identity compromise, supplier abuse, SaaS data theft, data extortion and customer account takeover.

- Start post-quantum migration with inventory: focus first on discovery, dependency mapping, vendor engagement and crypto-agility.

Conclusion

The cyber threats facing financial institutions in 2026 are increasingly difficult to treat as separate categories. Ransomware, fraud, supplier compromise, identity abuse and state-aligned activity often depend on the same conditions: valid access, weak verification, exposed services, shared technology providers and incomplete visibility across business processes.

Reducing the risk of a cyberattack in the financial sector is about understanding how incidents actually develop inside a financial institution. Where can an attacker gain access? Which systems or workflows would let that access become consequential? Which teams would need to act, and how quickly would they have enough information to do so?

The institutions best prepared for 2026 will be the ones that can answer those questions with evidence, not assumptions.

FAQ

What are the biggest cyber threats to financial institutions in 2026?

The biggest cyber threats to financial institutions in 2026 are ransomware and data extortion, identity compromise, third-party and supply-chain attacks, AI-enabled fraud, hacktivist DDoS, customer account takeover and state-aligned activity. These threats matter because they target the trust points financial firms depend on: identities, payment workflows, digital banking channels, SaaS platforms, cloud services, vendors and customer-facing financial systems.

What is the biggest cyber threat to banks in 2026?

For banks, the most material cyber threat in 2026 is the combination of identity compromise, ransomware-driven data extortion and third-party technology exposure. Attackers increasingly gain leverage by stealing valid credentials, abusing remote-access systems, compromising SaaS environments or exfiltrating sensitive data before any encryption takes place.

Which ransomware groups are most relevant to financial institutions?

Akira is one of the most relevant ransomware threats to financial organizations because of its use of VPN access, valid credentials, exposed services, known vulnerabilities and data exfiltration. ENISA also identifies Datacarry and BlackLock as ransomware strains reported against EU financial institutions. More broadly, financial firms should focus less on group names and more on the common attack paths: exposed remote access, weak MFA, unpatched systems, credential theft and data extortion.